@AP911_Studio/shutterstock.com

@AP911_Studio/shutterstock.com

The Labor Shortage was listed as the #5 Issue in the 2023-24 Top Ten Issues Affecting Real Estate® by The Counselors of Real Estate®.

Everyone, everywhere, in nearly every sector is reporting that it is difficult to find skilled, willing and able workers. Layering on top of the worker shortage are a series of trends that are changing requirements for both workers and employers.

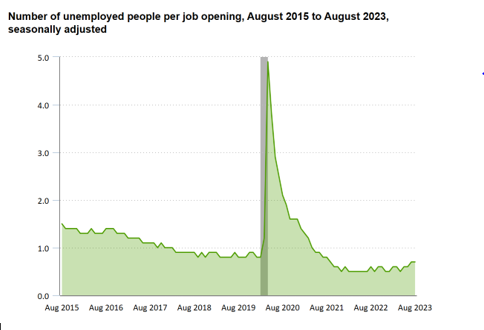

Despite some signs of softening in the wake of Federal Reserve rate hikes, the labor market remains incredibly strong. The monthly Job Openings and Labor Turnover Survey (JOLTS) report consistently shows more job openings than there are available workers. On the last business day of August 2023, there were 9.6 million job openings and 6.4 million unemployed people. This yielded a ratio of unemployed people to job openings of 0.67 for August, unchanged from July. The ratio of unemployed people per job opening has been below 1.0 since May 2021, and the July and August 2023 figures are the highest since September 2021. The number of unemployed people per job opening peaked at 6.5 in July 2009, immediately following the Great Recession. Publication of this data series began in 2000.

The biggest factor contributing to the labor shortage is the aging population of baby boomers that are moving out of the workforce. That labor shortage was accelerated during the pandemic with more people who left the workforce with the Great Resignation.

According to the American Association of Retired Persons (AARP), in 1958, 9% of Americans were 65 and older, totaling about 15 million. By 2023, that swelled to 17% of Americans being 65 and older, totaling almost 55 million. Many Americans are now working long past the traditional retirement age of 62, either by choice or economic necessity.

Additionally, the rising cost of childcare impacted families with two-income households. The choice to stay or work from home to take care of children became a larger issue as the country emerged from the pandemic.

Employers are struggling to not only find workers to fill jobs, but also keep up with a dynamic labor market that is moving at a fast pace. Over the last five years, the American workforce has not stayed static. Data from the National Occupational Employment and Wage Estimates put out by the U.S. Bureau of Labor Statistics (BLS) tracks the fluctuations in the labor market. In 2022, the U.S. population stood at 333 million. As of October 30, 2023, the U.S. Population grew to 335,651,924 as the third most populous country behind China and India, according to the U.S. Census Bureau.

The labor market has and will continue to shift, and the change is accelerating faster than the data can keep up. The dislocation in the workforce goes beyond just demographic changes with an aging workforce and continued population growth to include changes in technology, migration trends and changes in worker behavior.

Game changing trends

The pandemic was a game changer. At its peak, 62% of all office workers were working remotely, which introduced new virtual ways of working. Many of those workers are continuing to demand more remote work options. They like the convenience and flexibility, not to mention saving time and cost on a tedious commute. The office has relocated to the home or apartment, and the U.S. office markets have been greatly impacted by this dynamic.

A variety of reports using different data sources and methodologies provide insight. According to the Colliers 2Q2023 Office Market Report, “The softening in key U.S. office market fundamentals, seen in the prior two quarters, continued in the second quarter of 2023. As a result, net absorption remained negative, while vacancy and sublease space hit new record highs. The U.S. office vacancy rate stands at 16.4%, an increase of 30 basis points in the second quarter. Vacancy has inched above the prior peak of 16.3%, seen at the height of the Global Financial Crisis, with further upward pressure expected to follow. On an encouraging note, net absorption, which measures the change in occupied office inventory, was positive in 37% of the metro office markets tracked in the national survey, up from 24% in the first quarter. National office net absorption totaled negative 14.4 million square feet, compared to negative 25.4 million square feet in Q1 2023.”

Technology also is changing work beyond just the traditional office worker. For example, telemedicine allows virtual visits with doctors and other health professionals. Self-service kiosks are reducing the need for workers in the hospitality and service industries, while automation and robotics are replacing human capital in assembly, warehouse and distribution facilities. Looking at what’s ahead, AI is the big elephant in the room. It is not yet clear how AI and machine learning might impact how work is done, job growth or declines across different industries and skills that will be needed in the future. AI is expected to have a significant impact on the labor force in the coming years. According to a report by Morgan Stanley, “AI is estimated to affect about 44% of the labor force in the next few years, with an economic impact of 4.1 trillion dollars.” However, it is important to note that AI’s impact on employment is not entirely negative. A study by the Organization for Economic Cooperation and Development found that greater exposure to AI was associated with higher employment in occupations where computer use is high.

Jobs follow talent

Although the job market has been holding up under economic pressure, the bank failures that occurred early in 2023 are a warning sign that the Fed was slow to react to inflation and then perhaps overcorrected with its rapid interest rate increases. The question now is whether the U.S. will experience a soft landing or a hard recessionary landing. Labor markets often lag, and layoff announcements have started to emerge across many sectors, particularly tech. The labor market has significant downstream implications for real estate. Pure and simple, jobs drive demand for real estate, and populations also shift to where jobs are located.

Employers are following the people and paying close attention to migration shifts as they search for talent. Traditionally, older generations set up their lives around where their job was located. Younger generations, including Gen X, Y and Z, are now taking a different approach. They’re reversing the order, choosing their lifestyle and where they want to live first and the job second. Younger workers also have a different mindset as it relates to remote work and contract work versus full-time employment. They tend to be more entrepreneurial, and they might work two or three jobs. So, in addition to tracking the availability of labor, employers need to consider the shifts in attitudes, behavior and skillsets that are reshaping the workforce. The migration of the U.S. Population to the Southeast and Southwest and parts of the Midwest has companies expanding or relocating to the top inbound states such as Florida, Texas and the Carolinas.

Looking to the future

Site selection consultants now include housing availability and quality of life elements as part of their search criteria, as economic developers highlight the lifestyle assets their communities have to offer. And educational institutions are also taking note, as partnerships form with growing industries to attract talent. With a focus on placemaking and creating lifestyle experiences within communities, the labor market will steer real estate toward products and amenities that drive consumer and employee demand.